Global emissions are set to peak this decade, then fall to 2017 levels by 2030 and lead to a 3°C temperature rise by 2100 in a Reference scenario. To keep the 1.5°C target possible, massive investment in decarbonisation is needed in the current decade, according to a JRC modelling exercise.

The results show that energy sector investments need to increase by 70% this decade, reaching over $3 trillion by 2030, energy efficiency rates double, and renewables deployment reaches 11 TW by 2030 in the 1.5°C scenario. Scaling up investments in clean technologies compensates for declining investments in fossil fuels, boosting demand for investment across different sectors in the economy, such as the construction and manufacturing sectors. This requires a bigger workforce, in both direct jobs, and jobs across the value chain.

Published in the report Global Energy and Climate Outlook 2023, the findings show that the energy sector investment share in global GDP in the future remains broadly the same as today, indicating that the global economy can manage the burden of decarbonisation.

The report looks at investments in energy production, transformation, supply and demand and how they need to pick up pace during the current decade in order to align the global trajectory of emissions with a 1.5°C-compatible pathway. It also highlights implications for employment.

Energy supply: sharp investment growth that remains manageable

The upfront investment in many low-emission technologies is higher than their high-emitting competitors, however the total lifetime cost, including running costs, is often lower due to lower operating costs.

According to the report, annual spending on energy production and supply equipment increases by 70% this decade, rising from $2 trillion in 2022 to almost double by 2045, reaching $3.8 trillion, with a particularly sharp increase in clean power generation investment in the current decade.

But investment as a share of global GDP remains at the historical average of 1.4% through the projection period in the 1.5°C scenario, suggesting the financial burden is manageable. Reflecting the steep growth in investments this decade, the share of global GDP spent on energy supply increases throughout 2030 but then stabilises and decreases to become lower than today by 2050.

Clean energy technologies

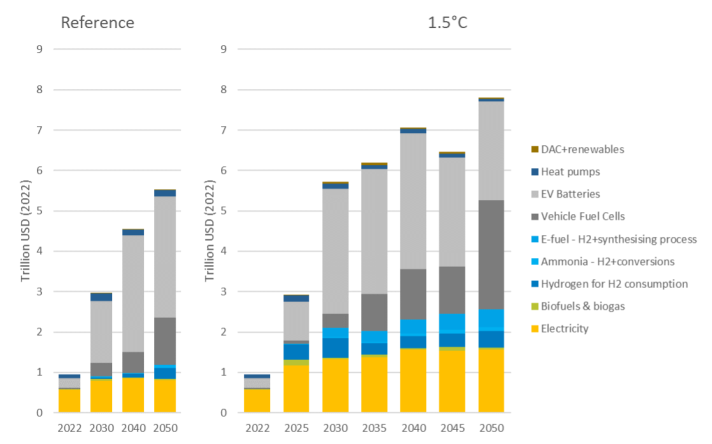

Global annual investment in clean energy technologies increases 6-fold from 2022 to 2030 in the 1.5°C scenario, up from $1.0 trillion today to $5.7 trillion in 2030. Annual investment in electric vehicle batteries expands 14-fold by 2030, representing the largest investment in clean technologies. It results from a 29-times increase in deployment by 2030 and a cost reduction of batteries of 60% by 2030.

Annual investment in clean technologies for electricity production double from 2022 to 2030. Annual new capacities of wind off-shore and on-shore increase by 8-fold and 2-fold, while unit costs are slashed by 16% and 20%, respectively. Total installed capacities of PV increase by 270%, which is offset by a decrease of unit costs of 35%.

Investments in hydrogen and hydrogen-derived fuels (e-fuels and ammonia) represent around a quarter of total clean technologies investments by 2050. Despite their minor role in the aggregate final energy consumption, these are crucial in decarbonising specific sectors such as aviation, shipping, and steel production and replacing grey hydrogen in fertiliser production.

The effect on supply chains and jobs

Increasing investments brings benefits beyond delivering the energy transition and its environmental and climate benefits. Higher investments in clean technologies compensate for declining investments in fossil fuels, boosting demand for investment across different sectors in the economy, such as the construction and manufacturing sectors.

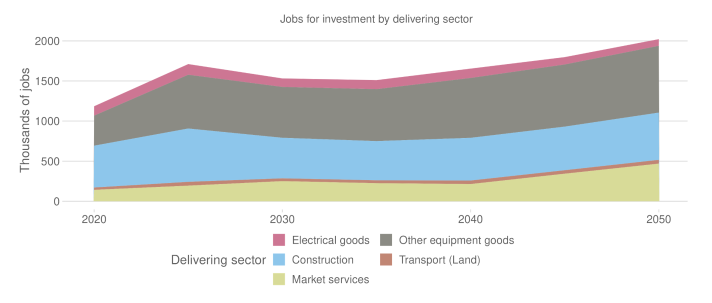

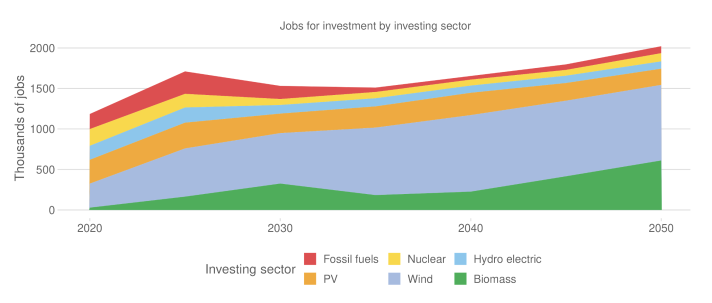

Changes in investments in different power technologies influence the jobs needed to make deliveries for investment, referred as indirect employment. While these indirect jobs decline over time for the fossil fuel sector, overall, there’s an increase in the number of indirect jobs created by investment in power technologies, caused by the expansion of renewables. From 2020 to 2050, there is a clear shift of indirect employment from the fossil fuels sectors to renewable.

Investment by the power generation sectors indirectly leads to employment mainly in the sectors concerning electrical goods, other equipment goods, construction, market services, and land transport. For investment by the power sectors, construction, and other equipment goods are the largest sectors delivering on investment needs.

By 2050 in the 1.5°C scenario, there is a total of 590 thousand jobs worldwide in construction for the power generation sector. Moreover, there is a total of over 800 thousand jobs in the ‘other equipment goods’ sector to produce power generation equipment.